factor&strategy »

涨到溢出!PEPE告诉我,大盘还能涨几多?

这两天涨得喜气洋洋的,不过,对东财的程序小哥哥来说,可能还得加班了,因为涨得太好,程序溢出了:

这是什么情况?

温故而知新

在2024年9月,我们曾发表《节前迎来揪心一幕!谁来告诉我,A股现在有没有低估?》 一文。在那篇文章中,我们使用了akshare获取了上证指数的市盈率数据,并通过分位数和趋势分析,探讨了当时A股市场的估值情况。

当时我们的结论是:

如果仅从分位数统计来看,当下的A股是低估的。但如果考虑到市盈率总体上一直处在上升的趋势,以及最近一年来PE与指数涨跌的背离情况,判断A股是否已经低估还存有疑问,应该纳入更多维度进行判断。

现在是2025年8月,差不多快一年了。从成交量来看,市场似乎进入了狂飙期。我们去年使用过的技巧,是否还能用来预测未来的走势呢?

还是让数据说话。

使用 Tushare 获取指数市盈率

Tushare上周给我们放了一个假。不过,还好现在已经恢复了。要获取指数的市盈率,我们需要用到函数index_dailybasic。

import pandas as pd

import matplotlib.pyplot as plt

import matplotlib.dates as mdates

from datetime import datetime

pro = pro_api ()

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29 def get_index_pe_close ( ts_code = '000001.SH' , start_date = '20100101' , end_date = '20250825' ):

# 获取指数PE数据

df_pe = pro . index_dailybasic ( ts_code = ts_code ,

start_date = start_date ,

end_date = end_date ,

fields = 'trade_date,pe_ttm' )

df_pe . rename ( columns = { 'trade_date' : 'date' , 'pe_ttm' : 'pe' }, inplace = True )

df_pe [ 'date' ] = pd . to_datetime ( df_pe [ 'date' ])

df_pe . set_index ( 'date' , inplace = True )

# 获取指数收盘价数据

df_price = pro . index_daily ( ts_code = ts_code ,

start_date = start_date ,

end_date = end_date ,

fields = 'trade_date,close' )

df_price . rename ( columns = { 'trade_date' : 'date' }, inplace = True )

df_price [ 'date' ] = pd . to_datetime ( df_price [ 'date' ])

df_price . set_index ( 'date' , inplace = True )

# 合并数据

df = df_pe . merge ( df_price , left_index = True , right_index = True , how = 'inner' )

# 排序

df . sort_index ( inplace = True )

# 移除PE为空的记录

df = df . dropna ( subset = [ 'pe' ])

return df

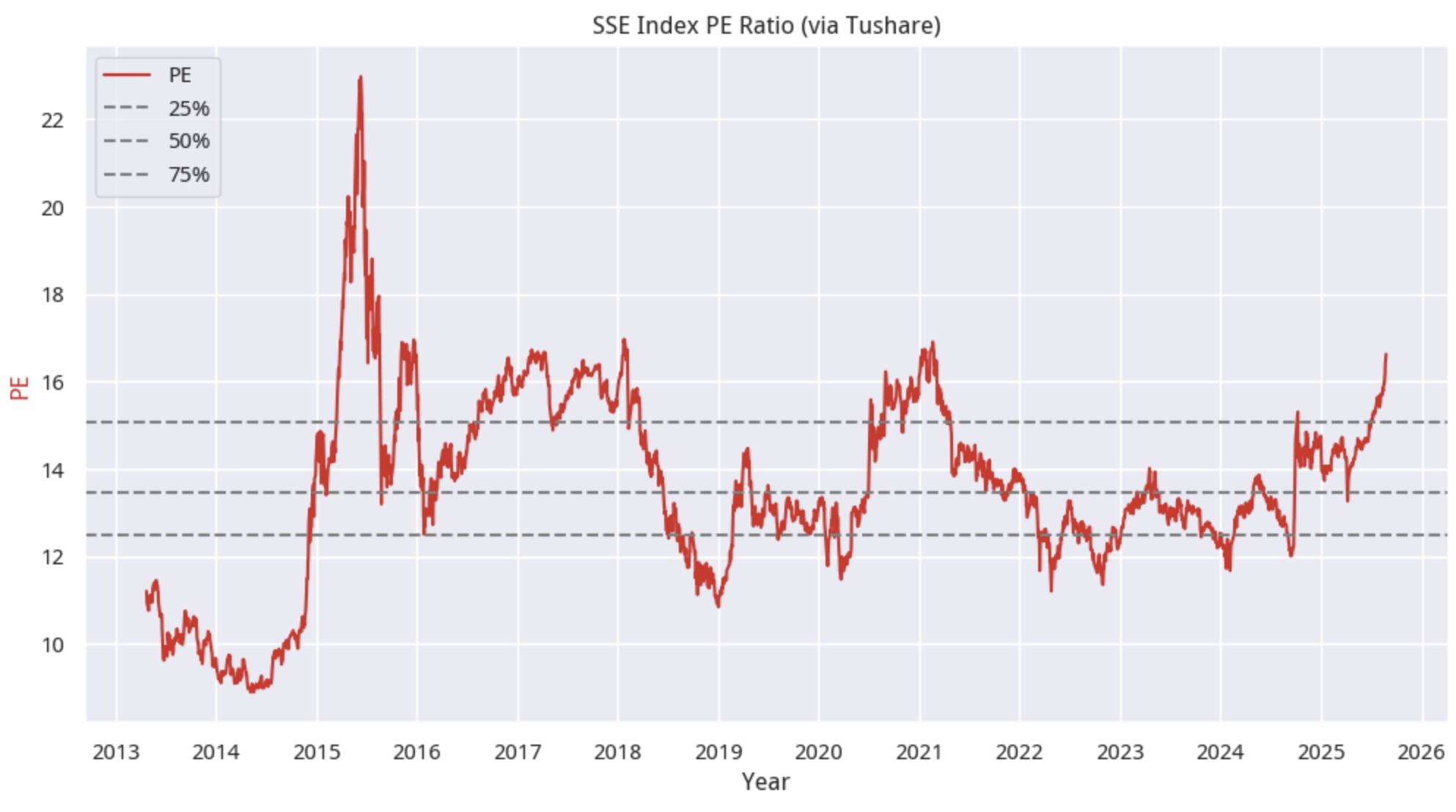

得到 pe 数据之后,让我们先来看一下直观走势:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21 # 绘制PE走势图

fig , ax = plt . subplots ( figsize = ( 12 , 6 ))

color = "tab:red"

ax . plot ( df . index , df [ "pe" ], label = "PE" , color = color )

ax . set_xlabel ( "Year" )

ax . set_ylabel ( "PE" , color = color )

ax . xaxis . set_major_locator ( mdates . YearLocator ())

ax . xaxis . set_major_formatter ( mdates . DateFormatter ( '%Y' ))

df = get_index_pe_close ( start_date = "20100101" )

# 添加分位数线

for i in range ( 1 , 4 ):

quantile = df [ "pe" ] . quantile ( i / 4 )

ax . axhline ( quantile , color = 'gray' , linestyle = '--' , label = f " { i / 4 : 02.0% } " )

plt . title ( "SSE Index PE Ratio (via Tushare)" )

plt . legend ( loc = "upper left" )

plt . grid ( True )

plt . show ()

数据表明,如果我们忽略2015年那段癫狂的历史(场外融资加杠杆),那么现在的 PE 水平已经是相当高了。

到底有多高呢?

def show_pe_quantile ( df ):

# 计算当前PE分位数

current_pe = df [ 'pe' ] . iloc [ - 1 ]

rank = df [ 'pe' ] . rank () . iloc [ - 1 ]

percentile = rank / len ( df )

print ( f "当前PE分位: { percentile : .2% } " )

show_pe_quantile ( df )

df = df [ df . index > '2016-01-01' ]

show_pe_quantile ( df )

如果从2013年起(tushare 似乎没有更早的数据了)开始算,那么当前PE分位数为95.18% ;如果从2016年1月起算,那么当前 PE 分位数则已达到98.81% ,很快就要满分了。作为指数来讲,确实是有点高了。

当前的 PE 值,是多少天以来的最高值呢?通过 pandas 可以很容易计算出来:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18 def find_days_since_max_pe ( df ):

"""计算当前的PE是过去多少天以来的最大值"""

if df . empty or len ( df ) < 2 :

return None

# 获取当前PE值

current_pe = df [ 'pe' ] . iloc [ - 1 ]

# 找到当前PE值在历史数据中的最大值位置

max_pe_idx = df [ 'pe' ] . idxmax ()

# 计算距离最大值日期的天数

current_date = df . index [ - 1 ]

days_since_max = ( current_date - max_pe_idx ) . days

return days_since_max , max_pe_idx

find_days_since_max_pe ( df )

答案是,现在的 PE 值是2018年1月24日以来的最大值,也就是创了7年来的新高。

假设指数能稳住,那么能让 PE 回到安全区的惟一答案,就是要靠企业利润增长了。如果指数就停在这个位置,要让 PE 回到安全区,需要企业利润增加多少呢?

我们通过下面的方法来计算:

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33 def required_earnings_growth ( df , target_percentile = 0.75 , target_index = None ):

"""计算使PE分位数降到目标值所需的盈利增长百分比"""

if df . empty :

return None

# 获取当前PE值和当前指数点位

current_pe = df [ 'pe' ] . iloc [ - 1 ]

current_index = df [ 'close' ] . iloc [ - 1 ]

# 如果指定了目标指数点位,则计算在该点位下的目标PE值;否则使用数据框中目标分位数对应的PE值

if target_index is not None :

# 根据PE = Price / Earnings,计算目标指数点位下的PE值

# 假设盈利不变,目标PE = target_index / (current_index / current_pe)

# 即 target_pe = target_index * current_pe / current_index

current_pe = target_index * current_pe / current_index

# 计算目标PE值(目标分位数对应的PE)

target_pe = df [ 'pe' ] . quantile ( target_percentile )

# 如果当前PE已经低于目标PE,则不需要盈利增长

if current_pe <= target_pe :

return 0.0

# 计算所需盈利增长百分比

# PE = Price / Earnings => Earnings = Price / PE

# 要使PE从current_pe降到target_pe,需要:

# (Price / target_pe) / (Price / current_pe) - 1 = current_pe / target_pe - 1

required_growth = ( current_pe / target_pe ) - 1

return required_growth

required_earnings_growth ( df )

通过计算可知,在现有的指数上,如果要让 PE 回到75%分位以下,那么企业利润需要增加10.2%。如果要让 PE 回到84.13%分位(即一个标准差)以下,那么企业盈利需要增长5.5%。根据企业的年利润增长水平,我们大致可以估算出这需要多少年。当然,这要求企业的年利润增长水平必须是正的。

如果我们希望指数能上涨到4000点,PE 还要回到一个标准差以下,那么企业利润必须增长8.68%以上。

情况就是这么个情况。总之,我们已经进入了『无人区』,没有数据可以利用了。

本文代码可以匡醍研究平台运行和下载。